INVESTMENT UPDATE FEBRUARY

| INDEX | LEVEL 31 DEC | LEVEL 31 JAN | CHANGE |

| S&P 500 | 4769 | 4845 | +1.59% |

| FTSE 100 | 7733 | 7630 | -1.33% |

| Euro Stoxx 600 | 478 | 485 | +1.44% |

| Nikkei 225 | 33288 | 36286 | +9% |

| Shanghai | 2962 | 2788 | -5.87% |

| US 10 Yr Treasury Yield | 3.86% | 3.96% | +0.10 |

| UK 10 Yr Gilt Yield | 3.54% | 3.78% | +0.24 |

| Bund 10 Yr | 2.02% | 2.16% | +0.14 |

Overview

In many equity markets, January saw a continuation of the progress seen in Q4 2023, with the US, European and Japanese markets seeing positive returns. Indeed, the latter (in local currency terms at least) posted near double digit gains – only the weakening Yen detracting (a weaker currency reducing returns for sterling investors).

However, in the case of fixed interest markets, we saw the opposite, as the realisation that perhaps the prospects for a significant number of interest rate reductions weren’t as likely as it seemed late in 2023. This realisation was aided by comments from Central bankers during January, who seemed keen to dampen the markets’ previous enthusiasm. This caused bond yields to rise in western economies, with a corresponding fall in prices (prices move inversely to yields). However, the net effect was to leave portfolios broadly flat for the month.

It should be noted that markets seemed to ignore the increased geopolitical risk, as tensions grew in the middle east, with clearly domestic matters seeming to be of greater concern. Whilst concerns exist over supply line times, crude oil prices have remained around the same level as, whilst it may take longer to divert deliveries from the Red Sea route, the actual cost of doing so is marginal in dollar per barrel terms. As the map showing the routes of container ships shows below, this is clearly happening:

Source: Steno Research, Jan 24

US

Once again, returns were dominated by those of the Magnificent 7, repeating a theme seen through the majority of 2023. Indeed, markets outside of the S&P 500, such as Mid and Small sized company indices, delivered negative returns, as they focussed on short term interest rate prospects. In US, the aforementioned enthusiasm for lower rate prospects was well and truly dampened by US Federal Reserve (Fed) Chairman, Jerome Powell, who suggested that the market’s view on both the timing of the first cut in interest rates and subsequent number of cuts priced in at the end of the year was way ahead of the Fed’s own expectations.

With the Magnificent 7 stocks, however, investors focussed on their earnings figures, which aside from Tesla, still seemed to support the still lofty valuations of those companies. Perhaps, as a warning to any of these companies disappointing in future on the earnings front, Tesla shares fell 25% in January as they reported slowing demand for their EVs. On the economy front, the US continued to exhibit impressive GDP growth even in the face of higher interest rates, and non-public sector employment rose less than expected, adding to the belief of some that the ‘goldilocks’ scenario of a non-recessionary slowdown, coupled with inflation reaching the Fed’s 2% target, might be achievable.

Powell’s comments suggested however that he was still focussed on current inflationary pressures, as the CPI (Consumer Price Index) for December came in at a slightly higher than expected 3.4%, although the Fed’s preferred measure, the PCE (Personal Consumption Expenditure) index, decreased to 2.93%.

Europe

European markets followed the pattern of the US, with equity indices moving ahead, led by technology related indices, whilst bond yields rose and prices declined. This may seem more incongruous than the US situation, where the economy remains strong, whilst the opposite applies in Europe.

It could be that the poor economic outlook, evidenced by the Manufacturing Purchasing Managers Index showing business activity declining for the 8th month in a row, stimulated optimism that this would put pressure on the ECB to reduce interest rates. Indeed, the consensus now appears to indicate that this will happen around April and thus earlier than now expected in the US, although rates were held at the ECB’s January meeting.

UK

The UK stock market continued to lag its western peers, with the broad FTSE 100 index delivering negative returns, with a similar picture for the gilt market. What was encouraging to see was the FTSE Mid 250 Index, comprising the next 250 companies by size, not losing any significant ground to its larger equivalent. Perhaps the relative valuation of the market and the continued strong pound playing a part.

Indeed, it is companies outside the main market that now seem to offer the better opportunities in general. On the economic front the Bank of England, as with other western central banks, held interest rates steady, particularly as UK service inflation remains elevated compared to other Western countries. Nevertheless, the BoE is now projecting 1% of rate cuts by year-end with inflation declining below 3%.

Japan

In Yen terms at least, the Japan stock market experienced an excellent start to 2024. Whilst it may have been a be a new year, the drivers behind the rise seemed to repeat those of 2023 i.e. speculation over improved prospects for the abandonment of the yield curve control* and increased foreign ownership as a result of better corporate governance implemented by the stock exchange. Indeed, foreign investors were net buyers of the market in 2023 for the first time since the end of 2020.

There still appear to be large disparities in company valuations, with growth companies still at a larger premium to value ones, so opportunities do still seem available on a selective basis. A strengthening Yen is a likely repercussion of the YCC abandonment and, whilst this may bring its own challenges for exporters, the prospect does make the currency an attractive prospect for overseas investors.

*Yield curve control (YCC) – for a number of years the Bank of Japan have been limiting the maximum yield available on their 10-year bonds by buying bonds in the market, thus limiting the return available.

Asia and Emerging Markets

China continues to struggle, and January marked the imminent demise of Evergrande, the colossal property developer with outsized debts totalling $300 billion, the biggest debt burden of any company in the world today. Evergrande could slide into insolvency with knock-on impacts to the Chinese economy.

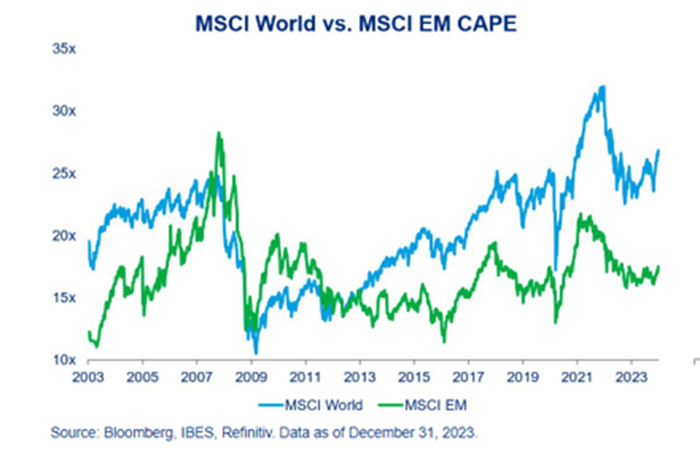

Stimulus is very likely to be provided by the People’s Bank of China to reflate economic activity during the months ahead. Elsewhere in the so-called emerging world, progress is undaunted by recession and prospects for a weaker dollar will add to forward momentum. Relative valuation seem to add some support to this prospect, especially when we compare the Emerging Markets (EM) index versus the rest of the World (CAPE is a measure of market valuation on an historical basis):

Outlook

We are in an election year in over 70 countries around the world in 2024. Of most interest, is that happening in the US in November, with the real possibility of Trump being returned as President there. Whilst, if this happens, it is likely to bring some challenges (it is already impacting Ukraine), the underlying liquidity environment is likely to be supportive to markets, with the Fed unwilling to be seen as partisan and the Democrats keen to maintain spending as voters head to the polls. It should be remembered that 80% of the time, an election year has been positive for the US market ending the year higher than when it began.

Elsewhere, we cannot ignore the possibility of further escalation in the Israel/Hamas conflict and its possible consequences, or even conflict between China and Taiwan, but such things are difficult to position for. But overall, we maintain a positive forward view for 2024, expecting equity markets to outperform bonds. That said, we are optimistic for bond yields to fall further and for the Dollar to weaken as the year plays out, supporting the move up in the broader base of more attractively valued stock. Our hedge on the dollar, now at around the 50% mark will likely continue to support progress.

Rockhold Asset Management, with contribution from Alpha Beta Partners and Marlborough, February 2024

Your Capital is at risk. Past performance is not a reliable indicator of future results. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances. Your capital is at risk and the value of investments, as well as the income from them, can go down as well as up and you may not recover the amount of your original investment.

.png)